We can't find the internet

Attempting to reconnect

Something went wrong!

Attempting to reconnect

VANNtastic! · 3.0K views · 200 likes

Analysis Summary

Ask yourself: “Did I notice what this video wanted from me, and did I decide freely to say yes?”

Pathos

Appealing to your emotions — fear, joy, anger, sadness — to make an argument feel compelling. Rather than persuading through evidence, it works by putting you in an emotional state where you're more receptive. The emotion becomes the proof.

Aristotle's Rhetoric; Kahneman's System 1 processing

Worth Noting

Positive elements

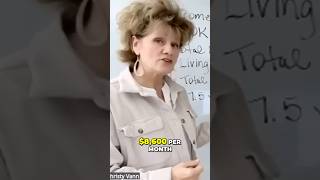

- Provides a specific, spreadsheet-based numerical walkthrough of applying Velocity Banking to a $92k multi-debt scenario, contrasting payoff timelines versus traditional loans.

Be Aware

Cautionary elements

- The example doubles as a soft endorsement priming purchases of the host's Velocity Banking courses and tools.

Influence Dimensions

How are these scored?About this analysis

Knowing about these techniques makes them visible, not powerless. The ones that work best on you are the ones that match beliefs you already hold.

This analysis is a tool for your own thinking — what you do with it is up to you.

Related content covering similar topics.

Beat Bad Credit

VANNtastic!

Stop Drowning in Debt Interest

VANNtastic!

High Income But STILL Negative Cashflow

VANNtastic!

Save Money WHILE Killing Debt

VANNtastic!

First Lien HELOC - The Basics - Replay

VANNtastic!

Transcript

This was super exciting for him. I hope it's super exciting for you. Let's just run the numbers and let the math do its work. We're just doing math. Uh you can do it in your own finances and you're going to be super super excited how these lines of credit work. If this is your first time seeing the videos on the lines of credit, the line of credit can be at the same bank as your checking account. Okay? And when your income comes in, when my income comes in, I transfer it manually into my line of credit. When I need money, like to pay gas, electric, phones, whatever, I can transfer it right back out and put it into my checking as I need it. What does this do? Well, the income going in keeps the balance low on the line of credit so you're not paying so much interest, right? Can you do that with a loan? Can you throw, you know, your income into a loan and then say, "Okay, now I need to pay my phone bill. Let me have, you know, $200." No. The line is revolving. So, your income can go in, then your expenses come right back out. You've always got money to work with. It's so easy to live out of these lines and it's super exciting because it pays off your debt fast. Now, let's go back to this guy and let's total up what I have here in his expenses. So, he has 27,000 for the home and the 17,000 for the second mortgage and then 3,000 for one car, 30,000 for the other, 8,000 in credit cards, and 7,000 in a personal loan. So $92,000 is his total debt besides that uh retirement loan, whatever that was. So that means that he had 550 in payments on the home mortgage 275. One car 722 the other car 300 in the credit cards 434 and the personal loan and 700 2981. Yeah, I was going to say the payment on the IRA comes up to almost $1,000, whatever he did there. So, this total debt payments is 29.81 for these debts. Okay. So, I'm going to change that because somebody out there is going to say to me, "Yeah, but you have 3,800 up there and you've only got 29.81." So, we're just going to change this around a minute. Okay. All right. So, let's run the numbers and see what happens. Do you tell me what do you think happened when he transferred these debts into this one line of credit? What do you think happened? All of these payments, what happened to them when he transferred it into the line? Poof. What? All of a sudden, he has $2,981 in cash flow that he didn't have before. Christy, how could that be? I know, right? Okay. So, all of these debts were paid off into the HELOC. All of a sudden, he's like, "Holy moly, I have almost $3,000 in cash flow when I had zero before." Okay, so how does he pay off this HELOC now? Because somebody out there is saying, "Yeah, but now he's got that big debt in the heliloc. How's he going to pay that off? What about the interest?" Okay, let's talk about it. His interest was 6.5% on this heliloc, but I'm going to calculate this interest at 10%. Let's do it at 10% for all of you guys who are saying, "Oh, the heliloc interest is so expensive. Why would she even suggest that?" I mean, he was only paying 2.5% on his mortgage. I know, right? Uh oh, he's only paying 7% on his car. I know. Oh, wait. He was only paying 8% on this personal loan. Okay. Okay. So, he has this right here had 22 years left on it. Yeah. High interest. The mortgage 27,000. I don't even know if I remember when that one was almost over. But if you just do the math, 27,000 divided by 550, if he doesn't pay any interest, which we know that's a lie from the devil, but let's act like he doesn't, he still has 49 months on just the mortgage. Okay? So, if he's got well over 10 years on some of these debts and then he's got five years on most of the others except for the mortgage, let's see how long it's going to take him to pay off the line of credit with the same money that he was paying out here. Okay. Oh, and what about this car loan that he he got seven years? Okay. So, let's see what happens when the income goes in. And remember, this is his income 6,800. And it doesn't matter how you're paid, daily, weekly, bi-weekly, monthly, whatever. As long as your income goes into the line, be 85 to 100. Okay. And now we have to pay his expenses because he's going to have expenses, food, gas, all that fun stuff. And let's add in the debt. So, we still since I only put a portion of his debt in here, we have to calculate how much his other payment is. So, let's see what that is. We have to add. So, $819. So, we'll add $819 that he has to pay out on the loan. Okay. So, let's add these up first. So, 85 to 100, 819, and 30,000. 8909. Now we have to add some interest. So the lines of credit are calculated on the average daily balance. Okay. But I am going to take it off of the high balance. 92,000 times 10%. Remember I'm charging high. His was only what I say it was 6.5%. I'm charging 10% to show you that it could still work with a higher interest. Let's see what we've got. So, let's say the first month is $767 in interest only. All right, let's run some numbers here. So, 89786 would be his balance at the end of the first month going into the second. Let's have his income go in here again. Income two. So 82 986 then we're going to add the expenses again the loan again. So that's 3819 total for expenses in a month and then let's calculate his interest. So we'll take the high the 89786 times 10%. You better not be getting a heliloc for 10%. That's very expensive. So let's say it's 748 in interest. So 87 553 going into the third month. So I could sit here and run numbers all day long. How long do you think his payoff is? Well, let's do some numbers. Remember, he paid off all of this debt. He no longer has it. It's gone. Yay. He no longer has these debt payments. He only has one loan payment now. And we could have put that in here and it would have made his numbers go faster, but he wasn't sure how he was going to, you know, if they would allow him to pay that off or not. So, I just wanted to make sure. So, 87 553. How do we know how long it's going to take him to pay this off now? Well, he has his expenses $3,000 a month. He has that loan payment for a while. Uh his income is 6800. So income expenses and then we're going to average his interest. So, if his high interest was 6 or 767, I'm going to divide that by two to get an idea that his average interest throughout the payoff of the loan would be about $400. And let's see what kind of cash flow that gives him. $25.81 would be his cash flow. How long is it going to take him to pay off the 92,000? Well, you just divide the 92,000 by 25.81. 36 months. 36 months to do what that second mortgage was going to take 22 month uh years to do. He had seven years left in his car loan. Remember, he still had 49 months without interest left on his mortgage. And he can do it all with a 10% line of credit in 36 months. It's not magic, guys. It's math. How is the bank using and abusing you right now? What are you sitting there making payment after payment after payment after payment onto a debt that never seems to go down? Why? because they have so much interest stuffed in there that you can't breathe financially. And when you learn how to use the revolving line of credit instead of just throwing cash to a loan that never appears to pay off, you're going to be free. There's no way it can't happen. I'm not a financial advisor. I am a person who has lived the life of sucking debt, totally suffocated for the first half of my adult life. Money for nothing. Thank you, Lord, for the very first time I heard about Velocity Banking and using the line of credit because I have been free ever since. You're going to get free, too. When you learn that the way the tools at the bank work are different, of course they're going to be throwing the loan at you. Of course, why? It's a money-making business. There's nothing wrong with making money, but you are paying way more than you have to for the things that you want in your life. The home, the car, anything else that you can think to buy, buy it. But do it in a way that is going to pay for the stuff you need and not buy the bank a house first. When you buy a home through a mortgage, you are paying for the bank's house first and then you might get to pay for your own. At today's interest rates, you're going to buy them two homes before you get to pay for yours. That's not fair. These are available. Like I said, this 70 yearear-old man has sit in debt all of his life and for the first time is feeling like he can breathe financially. It's just so important that you get free and you realize that maybe your spending is not the problem. Maybe where people, you know, out here on YouTube are telling you to uh, you know, stop eating out, how about stop paying interest to these banks that you don't have to pay and have plenty of money in a month to go out and eat. Am I wrong in thinking that that may not be why you're broke is because you're eating out too much or you know your kids wanted a new name brand pair of tennis shoes for school. Wouldn't it be nice to have $120 to say, "Yeah, I can get you a pair of shoes like that for once this year." Maybe if your family decided to take a, I don't know, a vacation for once and you get to do everything you want to do on that vacation and spend, I don't know, $3,000 because you probably saved $10,000 in interest that year by just learning how to use the revolving line of credit. I'm telling you, it is a financial game changer when you realize that you do not have to be broke. When you realize that it's not your fault that you are broke. It could just be that you are literally doing exactly what you were told to do, and that was to get the loan or anything you need and start making payments. Just make the payments. They say make them on time so you can keep your credit score up. Make them on time, you know, so that you know, you don't want to you don't want to mess up your credit. Meanwhile, they're laughing all the way to the bank cuz they are the bank. So, I want you to get excited. I want you to realize that you're going to get free once you realize what the line of credit is and how it's different from the loan.

Video description

ONLINE Step by Step VANNtastic On-COURSE! https://vanntasticmethod.manus.space/ $100 Discount for a limited time using PROMO Code: VANN100 Attend My LIVE & IN-PERSON Event In South Carolina, April 17th-18th ⬇ https://vanntasticfinances.com/april ------------------------------------- ⬇WAYS TO CONTACT/WORK WITH CHRISTY VANN 📞Book Christy Vann Directly For A 1-1 Coaching Session: https://calendly.com/vanncwi 📧 Contact Christy On Her Website: https://vanntasticfinances.com/contact 📲 Contact Christy By Texting VANN to 855-687-7078 📝Download Christy's FREE VANNtastic Finances Worksheet: https://vanntasticfinances.com/resources 💻Christy's Main Website: https://vanntasticfinances.com 💰Register For An Upcoming Debt FREEDOM Webinar, Hosted By Christy! Learn How To Become Debt-Free: https://vanntasticfinances.com/max ------------------------------------- Join My YouTube MEMBERSHIP To Get MEMBER'S ONLY Videos, MEMBER'S ONLY Livestreams, Access to Recent Webinar Videos, and more! https://www.youtube.com/channel/UCIaCojIRGdFRF50_ICrZXGA/join ------------------------------------- 🤝CONNECT WITH MY TRUSTED PARTNERS & AFFILIATES BELOW* 🔑Check Out the VANNtastic VAULT Spreadsheet Software and Christy AI! https://www.byobvault.com/?via=christy Promo Code: VanntasticVault30 👉First Lien HELOC Lender https://flhambassador.com/christyvann/ 🏡Motivated To GROW Your Own Business, But Feel Stuck? Book A FREE Consultation With My OWN Marketing Coach, Alex Albarran: https://www.alexalbarran.com/vanntastic 🏦 INFINITE BANKING CONCEPT http://beyourownbank.com/cv-book ----------- *Affiliate Disclosure: Some of the links shared may provide financial benefit to Christy Vann. She acts as an independent affiliate of Unstung Marketing LLC and other companies, and may receive compensation, referral fees, or other consideration if you choose to purchase or use the referenced products or services. This does not increase your cost. Always do your own research before making any purchase or engagement decision. **Disclaimer: Christy Vann and her affiliates do not provide financial, tax, licensing, legal, or accounting advice. All information provided through this website, YouTube channel, or related platforms is for informational and educational purposes only. Any actions you take based on this content are solely your responsibility. By accessing or participating in this channel, you acknowledge and agree to these terms. All information is provided “as is,” without warranties of any kind, express or implied. In no event shall Christy Vann or any affiliated organization be held liable for any damages, losses, lost profits, or lost data, even if advised of the possibility of such damages.t no additional cost to you.